As we move through the final quarter of 2025, the San Mateo County real estate market continues to show remarkable balance. Despite ongoing national economic shifts, local housing activity remains steady, and in many cases, stronger than expected.

Falling mortgage rates, steady demand, and resilient pricing are shaping what could be a more optimistic finish to the year for both buyers and sellers. With luxury sales rebounding and overall inventory tightening, the Bay Area market continues to prove its long-term strength and desirability.

Whether you’re preparing to list, considering a move, or waiting for the right buying opportunity, this month’s data provides valuable insight into where the market stands and where it may be headed next.

Home and Condo Prices

Median house prices in San Mateo County rose almost 7% year-over-year in October, reflecting strong demand and limited supply. The median size of homes sold also grew by about 3.5%, showing that buyers are still prioritizing space.

However, condo prices told a different story — the median condo price fell about 4.5% year-over-year, a common pattern across Bay Area condo markets where appreciation has slowed compared to single-family homes.

Despite seasonal fluctuations, long-term trends continue to show steady appreciation, supported by strong job markets and limited new housing inventory.

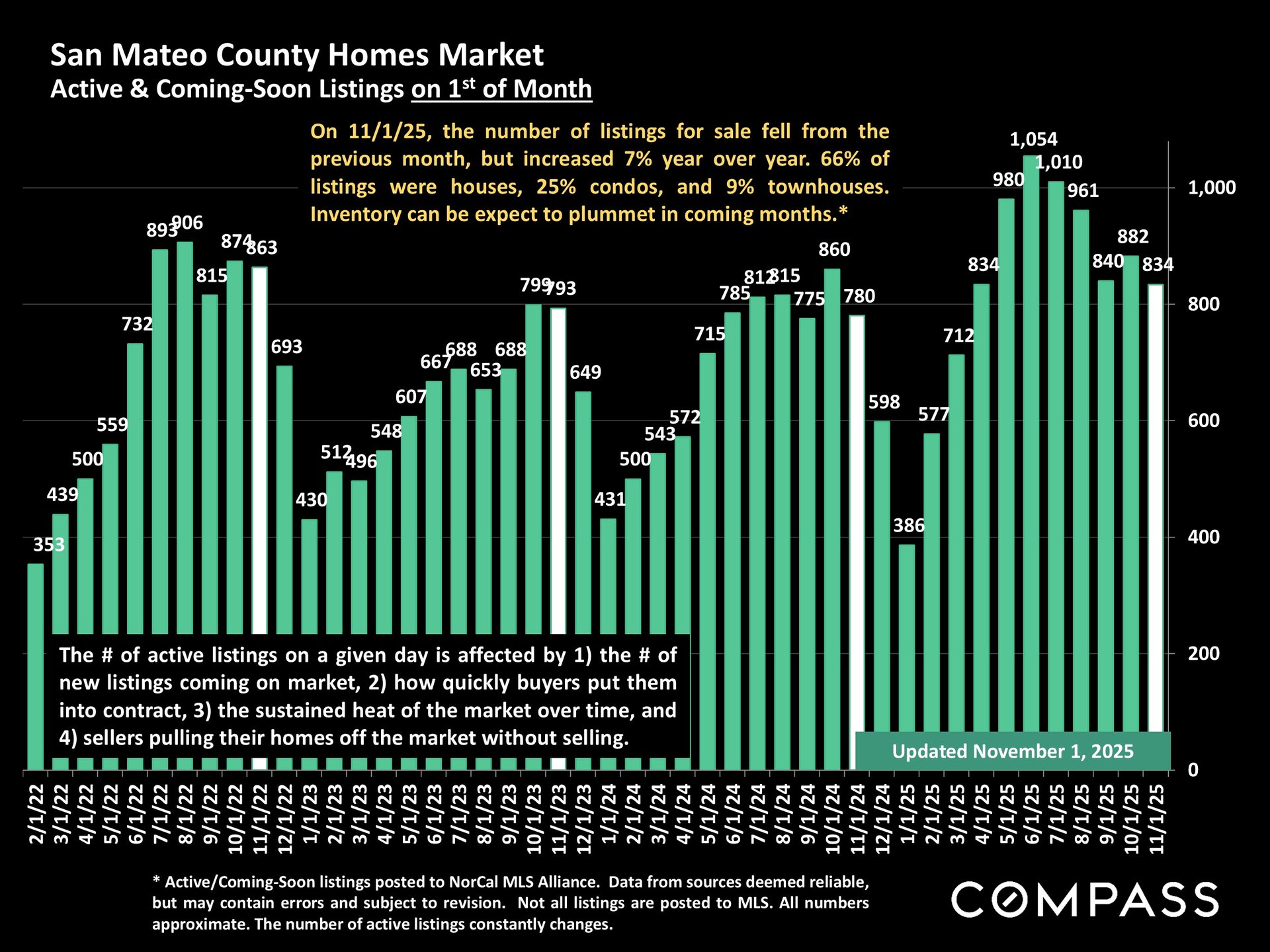

Sales Volume and Inventory

October saw the highest number of closed sales since spring 2022, up roughly 14% year-over-year. Luxury home sales above $5 million were especially strong, marking their highest October count on record.

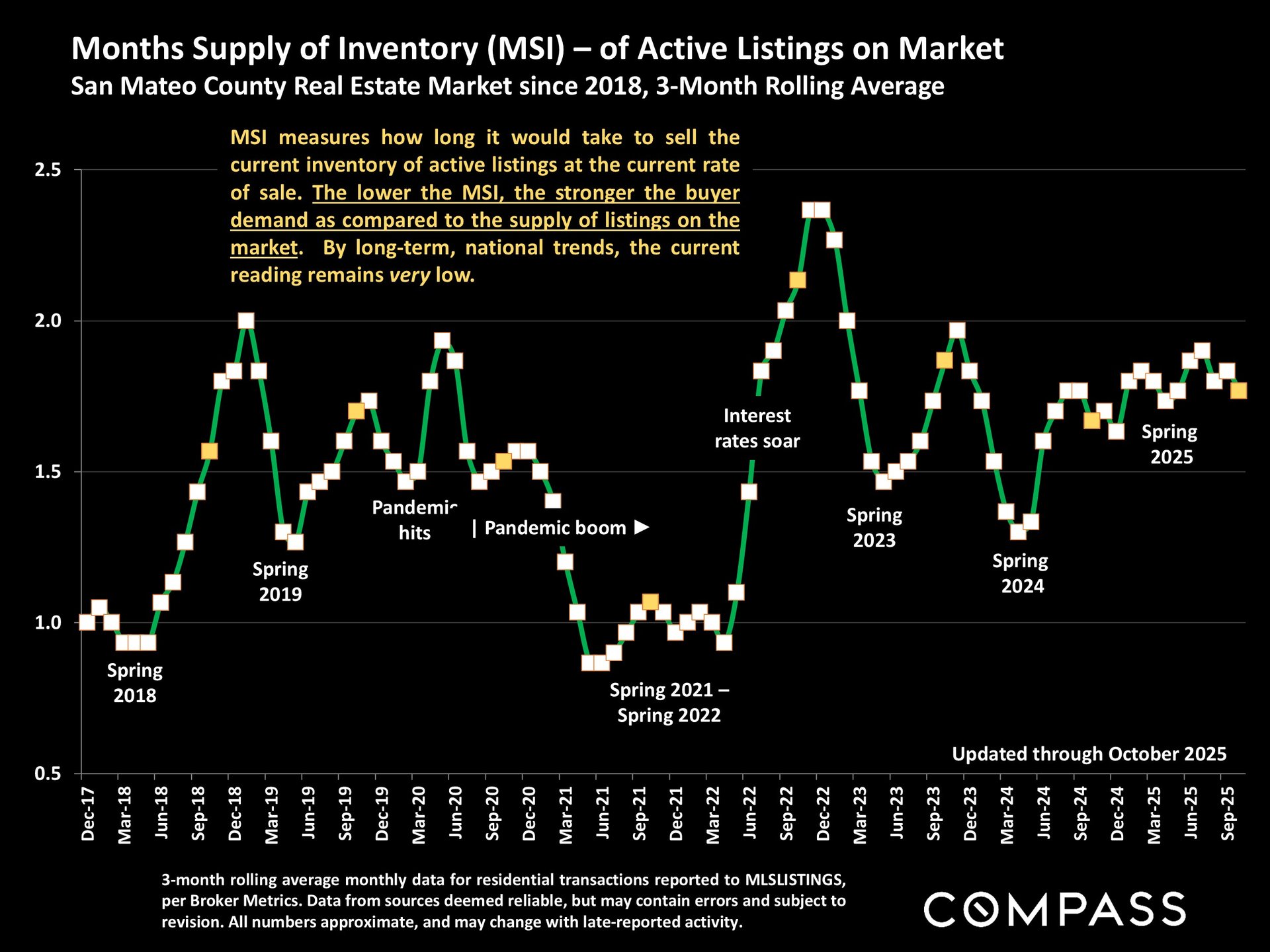

Inventory remains tight but improved compared to last year, with the number of active listings up about 7% from October 2024. Around 56% of homes sold for over asking price, indicating continued competition for desirable listings.

Looking ahead, inventory is expected to decline through the holiday season — a typical trend from mid-November to January — but motivated buyers and sellers may still see opportunities before year-end.

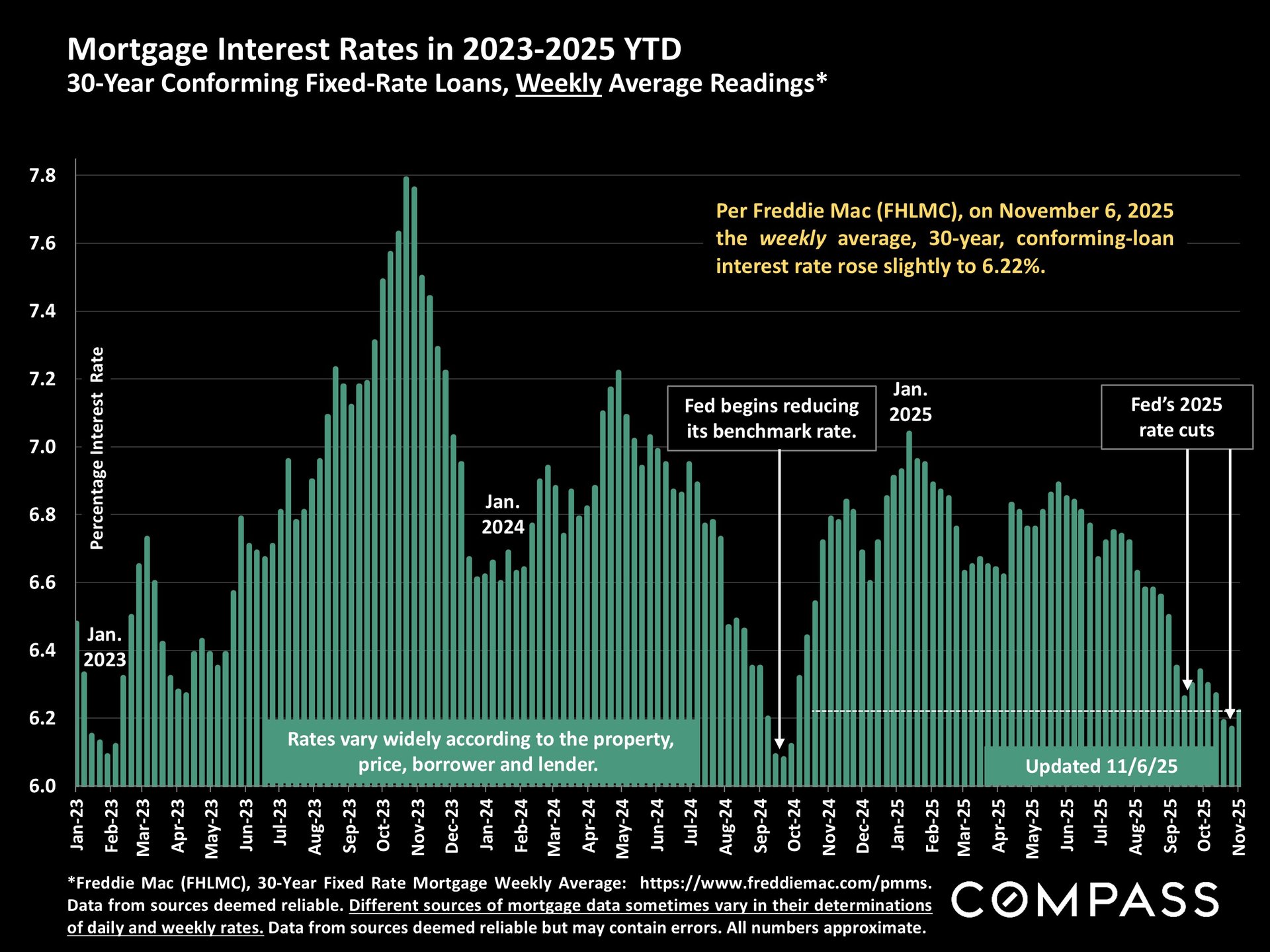

Interest Rates and Buyer Opportunities

As of early November, the average 30-year fixed mortgage rate settled around 6.22%, its lowest level since 2023. The Fed hinted at the possibility of another cut in December, which could further boost affordability and activity in early 2026.

This environment creates new openings for buyers who had paused earlier in the year due to higher rates. Sellers, in turn, are benefiting from renewed demand and shorter market times with houses averaging 26 days on market and condos around 59 days.

Key Takeaways

-

Prices remain stable overall, with houses up and condos slightly down year-over-year.

-

Sales are rising, reaching their highest levels since mid-2022.

-

Luxury homes are leading in activity, with record October sales above $5M.

-

Inventory is tightening heading into winter, which may keep competition strong.

-

Lower rates are fueling optimism and could set up a more active market in early 2026.

Whether you’re planning to buy or sell, understanding the timing and strategy is key in today’s evolving market.

Let’s Talk Strategy

If you’re curious about your home’s current value or want to explore what these shifts mean for your plans, I’d be happy to walk you through the numbers and opportunities in your area.