After several years of uncertainty, the housing market is finally starting to turn a corner. According to Compass’ 2026 Housing Market Outlook, we are entering a new phase where the market becomes more predictable, more balanced, and easier to navigate for both buyers and sellers.

The pandemic years brought extreme conditions. Prices surged, mortgage rates jumped quickly, inventory dried up, and many homeowners chose to stay put. Now, many of those distortions are slowly unwinding. While 2026 will not feel like a booming market, it does mark the beginning of a healthier and more stable environment.

Here’s what the data shows and what it means for you...

A New Housing Market Era Is Taking Shape

Compass describes 2026 as the start of a new housing market era. This does not mean the market suddenly becomes easy, but it does mean it becomes more functional.

Home sales are expected to grow again. Prices are no longer racing upward. Inventory is beginning to normalize in many areas. Buyers and sellers are adjusting expectations after years of shock and scarcity.

Instead of extreme swings, the market is moving toward balance, where decisions are driven more by life changes and long-term planning rather than fear or urgency.

Home Prices Are Expected to Stay Mostly Flat

One of the biggest questions heading into 2026 is what will happen to home prices.

Compass forecasts that national home prices will be essentially flat, with an expected increase of about 0.5%. The possible range runs from a modest decline to modest growth, depending on local conditions.

This would make 2026 one of the most stable price environments we’ve seen in years. Rising inventory and stretched affordability limit how much prices can grow, while strong homeowner equity and tight lending standards help prevent sharp declines.

This is not a repeat of 2008. The conditions that caused that crash simply do not exist today. Most homeowners have substantial equity, lending standards remain conservative, and there is no wave of risky loans resetting.

For sellers, this means pricing strategy matters more than ever.

For buyers, it means less pressure from runaway price growth.

Home Sales Are Expected to Increase

After years of suppressed activity, home sales are finally showing signs of recovery.

Compass expects existing home sales to rise by about 5% in 2026, assuming mortgage rates remain near current levels. If economic conditions improve further, sales growth could be even stronger.

Many households have delayed moves for years. As conditions normalize, that pent-up demand is beginning to surface. This does not mean a sudden surge, but rather a steady return of buyers and sellers who are ready to move forward.

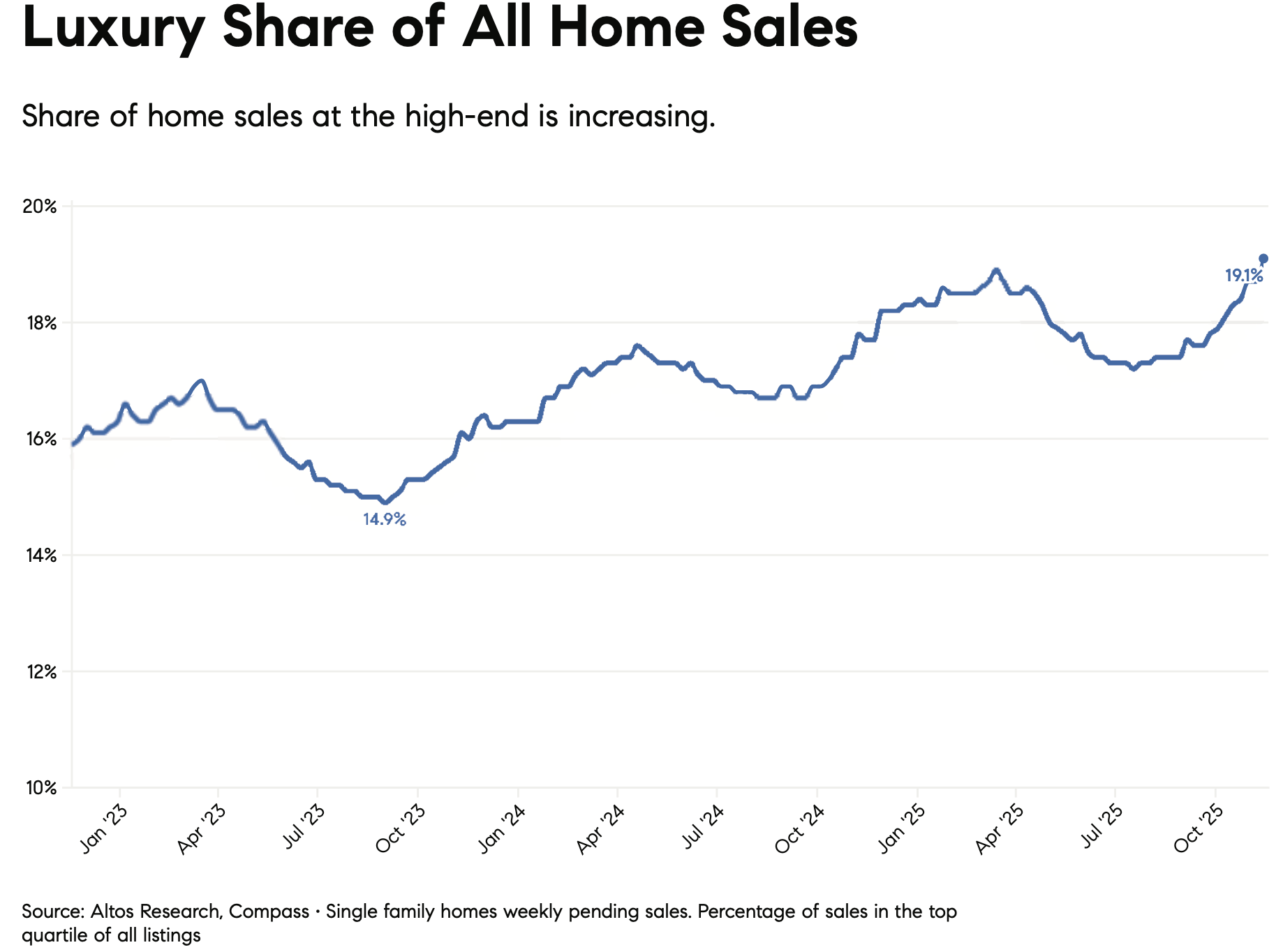

Luxury homes are expected to continue outperforming entry-level price points, largely because higher-income buyers are less sensitive to mortgage rates and often purchase with cash.

Inventory Is Finally Growing

Inventory has been one of the most challenging parts of the housing market, but 2026 brings meaningful improvement.

Compass forecasts approximately 10% inventory growth nationwide in 2026. Supply is increasing in many regions, especially as the mortgage rate “lock-in” effect fades.

This does not mean the market will be flooded with homes. Instead, inventory growth helps support sales activity and keeps prices from accelerating too quickly.

Regional differences remain important. Some markets still face tight supply, while others have more selection and longer selling timelines. National averages hide these local realities.

Mortgage Rates Will Likely Stay Elevated but Stable

Mortgage rates are expected to remain higher than the ultra-low levels of the pandemic years, but within a more stable range.

Compass expects mortgage rates to average around 6.4% in 2026, likely fluctuating between the high-5% range and high-6% range depending on economic conditions.

2026-housing-market-outlook

Mortgage rates have shown a clear pattern in recent years. When rates dip closer to 6%, buyer activity tends to pick up. When rates move higher, demand slows.

Even without a dramatic rate drop, affordability can still improve through flat prices and rising incomes.

Affordability Improves Gradually, Not Overnight

Housing affordability reached its worst level in nearly 40 years by late 2022. The outlook for 2026 is more encouraging, but improvement takes time.

Compass explains that affordability improves not through a dramatic price correction, but through a combination of flat prices, rising household incomes, and gradually easing mortgage pressure.

Incomes have been rising at a pace of about 4% per year, which slowly helps close the affordability gap. Lower mortgage rates would accelerate this process, but they are not required for improvement to continue.

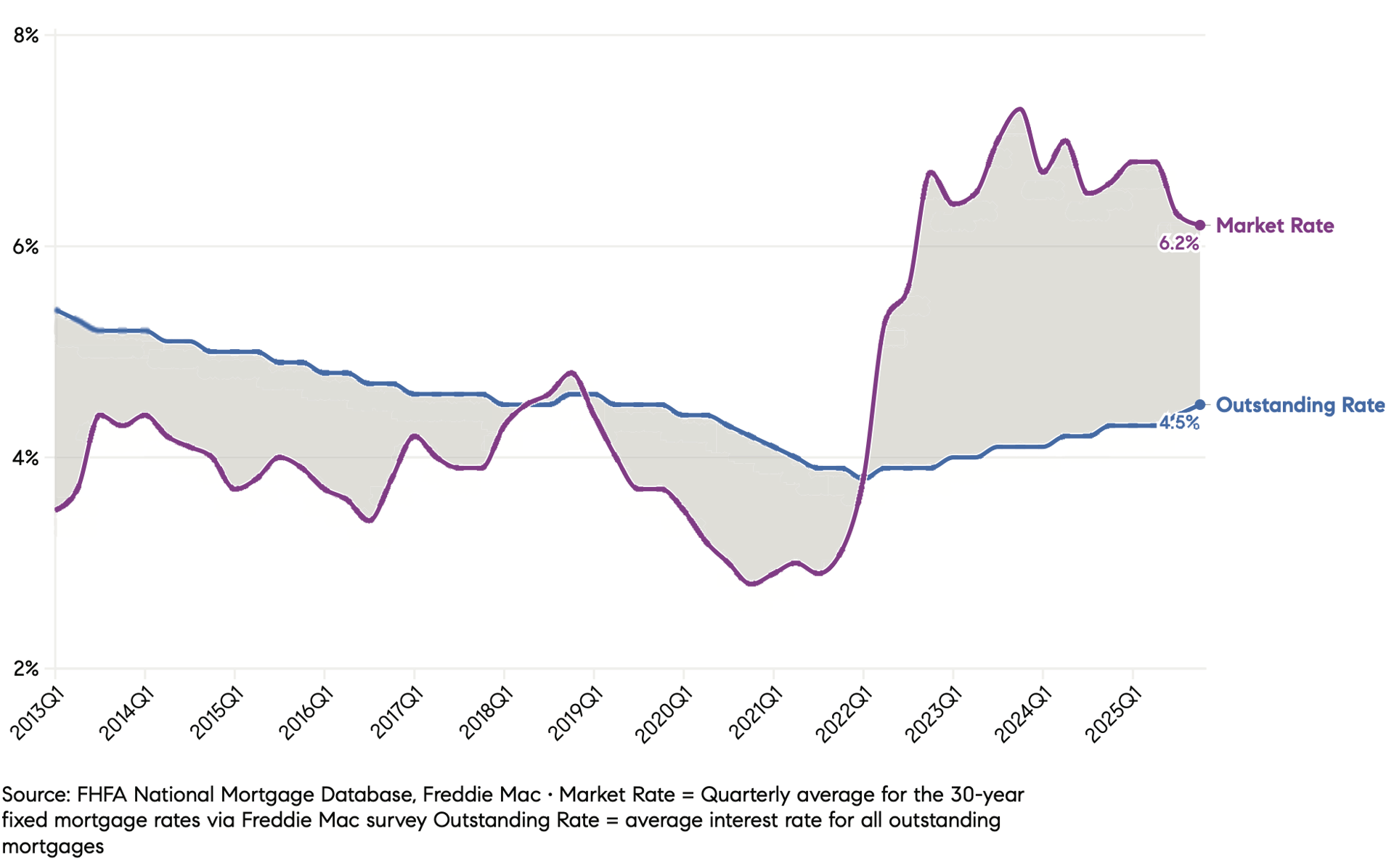

The Mortgage Rate Lock-In Effect Is Fading

One of the most important shifts heading into 2026 is the gradual end of mortgage rate lock-in.

During the pandemic, millions of homeowners locked in mortgage rates below 3%. When rates jumped, selling meant trading a very low rate for a much higher one, so many people stayed put.

That dynamic is changing. Nearly 20% of outstanding mortgages now carry rates above 6%, creating a growing group of homeowners who no longer feel financially frozen.

As lock-in fades, more homeowners are willing to move, helping unlock inventory and transaction volume.

Foreclosure Headlines Can Be Misleading

Compass notes that foreclosure activity may rise modestly in 2026, but context matters.

Even with an increase, foreclosure levels remain extremely low by historical standards and are nowhere near crisis territory. Most homeowners have significant equity and favorable loan terms, which greatly reduces systemic risk.

Some increase in foreclosures reflects normalization after years of artificially low activity, not a collapse in the housing market.

A Market Divided by Geography and Prosperity

One of the defining themes of 2026 is a divided economy.

Affluent households continue to benefit from strong financial markets and AI-related growth, supporting demand in certain regions and at higher price points. Meanwhile, younger and lower-income households face greater affordability pressure and job uncertainty.

This divide means national trends only tell part of the story. Some markets remain competitive, while others offer buyers more leverage and time to negotiate.

Understanding local conditions will be essential in 2026.

What This Means for Buyers and Sellers in 2026

For buyers, 2026 offers more options, less panic-driven competition, and better negotiating conditions in many markets. Timing, location, and financing strategy matter more than ever.

For sellers, success depends on realistic pricing, strong presentation, and understanding local demand. Homes that are priced correctly and well prepared will still attract serious buyers.

Overall, the market is not frozen and not overheating. It is becoming functional again.

Thinking About Buying or Selling in 2026?

National data provides helpful context, but real estate is always local. If you’re planning to buy or sell in 2026 and want to understand how these trends apply to your specific market, I’d be happy to help.

Reach out anytime to talk strategy, timing, or next steps with clarity and confidence.